English

English

français

français

العربية

العربية

Is Nigeria becoming uninvestible for foreigners?

- 07 June 2022 / News / 437 / Fares RAHAHLIA

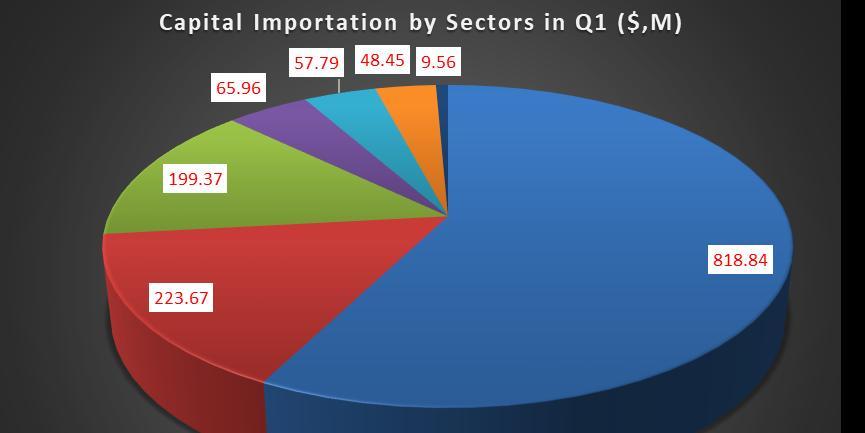

As envisaged, first quarter (Q1) capital importation data came last week with most of the figures in red. For the entire quarter, the country attracted a total of $1.57 billion. On year-on-year (YoY) analysis, the figure slumped by 17.46 per cent while the quarter-on-quarter (QoQ) performance was even worse at -28.09 per cent.

Nigeria’s capital importation has been on a slope in the past three years, from $23.99 billion in 2019 to $9.66 billion in 2020 (during the height of COVID-19) and further down to $6.7 billion last year. From the beginning of the year, it was obvious this was going to be a challenging year for Nigeria and other emerging markets that rely on foreign investment funds to grow their economies.

The tendency to align with the west was the first warning sign. The United Kingdom had started rolling back the era of low-interest rates last year just as the United States Federal Reserve System signalled an end to the pandemic-triggered expansionary monetary system to rein in inflation.

The World Bank and the International Monetary Fund (IMF) warned of a massive outflow of funds from developing countries. With the effective commencement of quantitative tightening by the Fed last week, the coming months could only be tougher for regions considered high-risk areas.

Just when the economy began to gain speed, Nigeria buckled under the weight of politics. In the past two weeks, for instance, the private sector has been effectively crowded out of the foreign exchange (FX) market by politicians who move about with briefcases shopping for dollars at any rate available.

Dr. Muda Yusuf, an economist and former director-general of the Lagos Chamber of Commerce and Industry (LCCI), said private sector operators simply do not have the wherewithal to compete with the war chest of politicians who spend ill-gotten money. Today, the premium on the black market exchange has widened to close to N200 per dollar, the worst in the history of the naira.

Experts believe this margin is a disincentive to foreign investors, who must sell their imported dollar at the Investors’ and Exporters’ (I&E) window where they will get an average of N415/$, a rate they scarcely get when they want to repatriate their profits. The Central Bank of Nigeria (CBN) mulled a rate convergence programme to deal with the consequence of the huge arbitrage about two years ago. But that has remained at the level of a plan.

Perhaps, this historical rigidity in the FX management process coupled with the unfriendly investment and rising political risk is threatening the country’s important source of FX – capital importation. The figures are low and falling but that is not much of a problem because of the uneven spread of the inflows.

The lopsidedness of the Q1 capital inflows figures may have reflected the ambivalence of policies and programmes of state governments with regard to attracting foreign investments. Sadly, only five states– Anambra, Katsina, Osun, Oyo and Lagos and the Federal Capital Territory (FCT), which comprised 71 per cent of the imported capital, attracted the entire inflow.

If this were to happen, it could be disregarded as white noise. But it has only stretched a historical trend to a frightful point. Last year, only 13 states assumed values in the country’s capital importation data while the figure was eight in the previous year.

Curiously, the entire oil-rich South-south is not represented in the Q1 data, raising a question about the attraction of the region to fresh investment. But for FCT and Katsina, the entire north would have been missing on the computation as well. Investment flow is a decreasing function of insecurity, and this is the point those who have warned about the long-term consequences of escalating insecurity, especially in the northern part of the country, have emphasized.

The asset classification of the capital is interesting where the country stands in global investment flows. Foreign portfolio investment (FPI), otherwise referred to as fair-whether or hot capital, makes up 61 per cent of the figure. Otherwise, foreign direct investment (FDI), which every economy needs to create jobs and develop, is 20 per cent. The rest is loans and other transient forms of capital. It suggests that while the capital inflow has fallen drastically, the bigger problem is the portion the country can key for medium- to long-term use is significantly low, a problem David Adonri, a financial expert, described as a major cause of the country’s external reserves.

Falling capital importation is a cause and effect of shrinking external reserves. In May alone, the country’s reserves went down by over $1 billion. And there is a panic that it could continue southward for the rest of the year, especially with heightening political tension.

The reprieve, however, may be a bullish export outlook. For the first time since Q3 2019, Nigeria recorded a trade balance in excess of N1 trillion last quarter. But there is little on the horizon to show if the country can tame the unrestrained imports, especially in the face of weakening production capacity and the rising cost of inputs. A strong industrial sector, perhaps, is an important factor in rolling back the painful impacts of a weak external sector. Unfortunately, with the cost of diesel at an all-time high and power still faltering, Nigeria does not seem ready to build resilient local industries.

source: guardian.ng